Over the past decade, interest in financial health or well-being has increased markedly among researchers, policymakers, activists, financial services professionals, and the general public. There is a growing consensus that identifying the drivers of financial well-being can help shed light on longstanding and overarching economic, health, and social challenges and inequalities.

What does well-being look like?

In 2020, interest in understanding financial well-being has become an imperative. The COVID-19 pandemic has impacted people’s physical and mental health, and it has attacked our social ties and connection to our communities. The recession has cost jobs and produced unthinkable uncertainty and instability in people’s lives and livelihoods. The social and political upheavals of the year—including a reinvigorated civil rights movement—have shown us how deep the inequities of our economy go.

In the midst of these dramatic changes, there has been a proliferation of studies of people’s finances—attempts to get under the hood of the weekly unemployment claims numbers, monthly jobs reports, and quarterly GDP growth estimates to better understand what, exactly, people are experiencing, day to day, week to week, month to month. What does financial well-being look like in practice? And can financial well-being tell us something about well-being more generally—something about people’s overall health, welfare, happiness, and prosperity?

The factors contributing to well-being are, by definition, perceptual and subjective, not necessarily nor immediately amenable to quantification. What may feel satisfactory to some may not be adequate or acceptable to others. It is tied to events outside of any one individual’s control, arising from events in the lifecycle or emerging from structural and systemic conditions and the broader, and ever-changing environment.

Even when it comes to calculating financial well-being, complications arise. Most now recognize that financial well-being is much more than financial literacy or education, more than financial capability, more even than financial inclusion. In “Pathways to Financial Well-Being,” a landmark report from Filene’s Reaching Minority Households Incubator, Filene researchers issued a call for credit union leaders to recognize that while access to affordable, responsible financial services is a critical piece of the financial well-being puzzle, inclusion is not enough.

The definition of financial well-being offered by the Consumer Financial Protection Bureau (CFPB), building on decades of academic and industry research, is a good starting place to build out a more comprehensive and holistic measure of financial well-being. According to the CFPB, financial well-being is “a condition wherein a person can fully meet current and ongoing financial obligations, feel secure in their financial future, and make choices that allow them to enjoy life.” Four factors are the critical ones: (1) having control over finances day to day and month to month, (2) having the capacity to absorb financial shock, (3) being on track to meet financial goals, and (4) having the financial freedom to make the choices that allow you to enjoy life.[1]

Filene’s Findings about Financial Well-Being and Credit Unions

Filene has a long history and deep archive of work on financial well-being and credit unions. Most recently, we have worked directly with credit unions on a series of customized research studies to help them better understand their members’ financial security, mobility, and stress and explore the connections between financial well-being and physical and social well-being. With these credit unions, we have baselined their members’ well-being and compared their members’ well-being with that of non-members who live in the same communities.

Credit unions are beginning to recognize the important role they already play in the financial lives of their members—and the opportunity they have to expand that role and, in doing so, differentiate their organization and deepen their engagement with members.

Credit unions can directly shape people's well-being by helping them increase their resource pool. Indeed, this is increasingly recognized as one of the most effective ways to elevate individual and collective well-being.[2] While credit unions may not be able to reduce all the challenges members face (e.g., an urgent car repair, an illness, loneliness), the organization can be an ally—not only as a service provider, but also as a coach, a custodian of resources, and an advocate—when circumstances inevitably change across people's lifecycles.

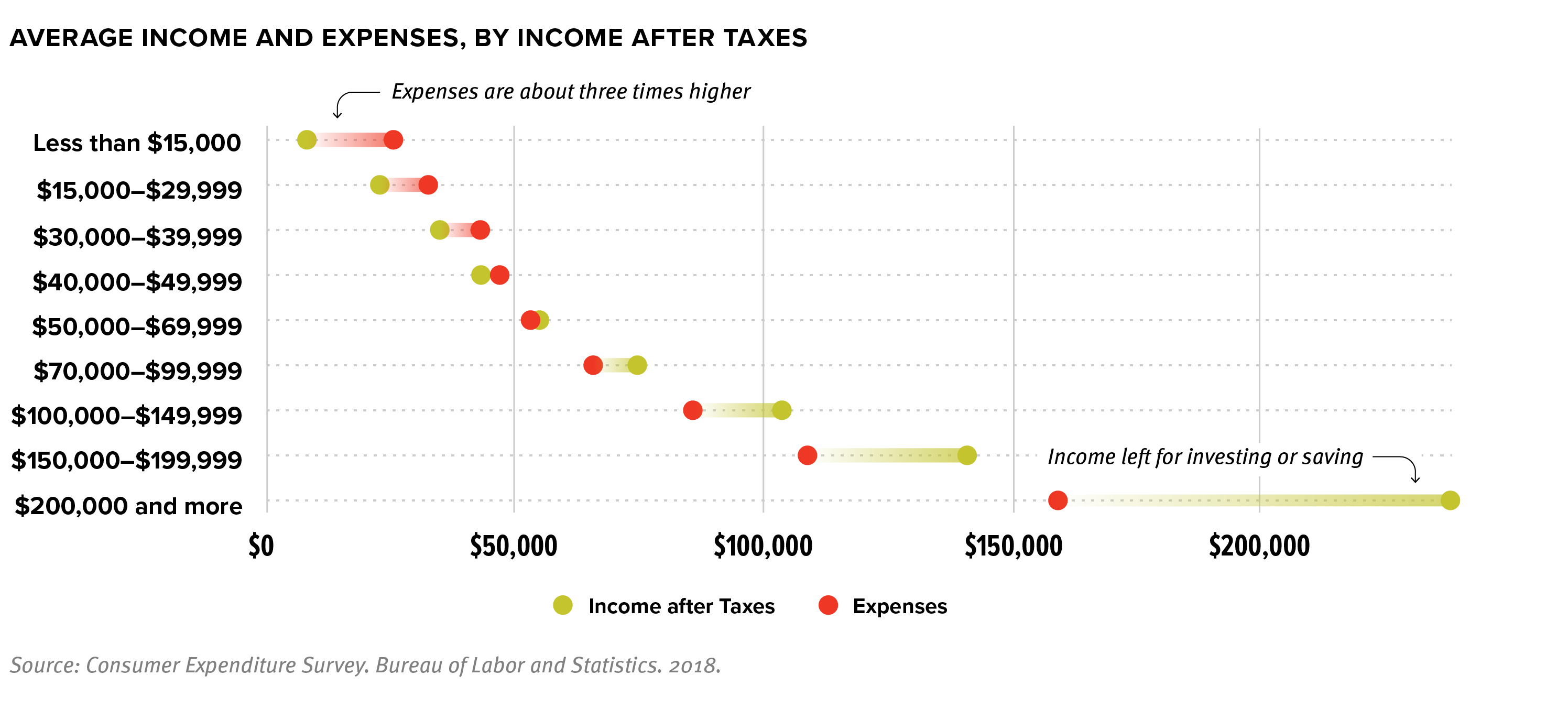

In our benchmarking research, we evaluate dozens of variables that can have an impact on well-being. Using the CFPB’s definition as a foundation, we look at the ways people manage their money and the links to self-reported perceptions of financial security and stress. Across geographies, the two factors we found that are most powerfully correlated with financial well-being are accumulated savings and confidence in borrowing.

Moreover, we also find strong correlations between financial well-being and physical and mental health, as well as different aspects of social life—people’s interpersonal relationships, or connections to the communities in which they live.

For example, individuals who report having “excellent” and “very good” health also report higher levels financial well-being levels. Indeed, 66% of people in the top quartile of financial well-being scores self-assess their health favorably. On the flipside, only a quarter of the people with financial well-being scores in the bottom quartile report the same.

Similarly, those individuals who participate in activities to make their community stronger and are satisfied with their social activities are three times more likely to be in the top quartile of financial well-being scores, with scores higher than 75% of respondents overall. The ratio of members in the top quartile of financial well-being that are not satisfied with their social relationships is only about one in ten, and only one in five individuals in the bottom quartile of financial well-being scores would rate their satisfaction with their social activities as “excellent” or “very good.”

There is, in short, a strong interdependence between financial, physical, and social well-being. Credit unions will be best served at identifying strategies that help members and the community achieve all three. Just as financial security can support physical and social well-being, improving access to health and living a healthy and socially rich life is a way of increasing prosperity.

Mental health adds another layer of complexity to well-being. Research conducted by the Kaiser Family Foundation discovered that as many as 53% of adults in the United States reported that their mental health had been negatively impacted due to worry and stress over the coronavirus.[3]

Our research has uncovered how such mental health struggles can also affect financial well-being. For example, individuals with lower financial well-being scores are also more likely to say that they feel fatigued, lonely, and depressed, and that they have difficulty making decisions.

What Credit Unions Can Do

Credit unions are uniquely positioned to support their members’ financial well-being, and our research shows that this can have widespread downstream effects on physical health and social life, too. So, what should credit unions do to jumpstart or advance their financial well-being efforts?

- Start measuring. Credit unions can and should baseline how their members are doing, and then track their progress—and, therefore, your own. This will allow you to check your assumptions, assess areas of need, and demonstrate to yourselves and potentially to your members what works.

- Focus on outcomes, not inputs. It might be tempting to assume that what your organization already offers—say, a financial literacy program, specially designed savings vehicles, or a payday alternative—is sufficient to support members’ financial needs. But what matters is not what goes in; what matters is what results.

- Focus on equity. Equity is not the same thing as equality. In an equal system, the same resources are distributed to all; but this does not take into account the fact that people are often starting in different places, and equal distribution is not enough to close historical gaps or remedy systemic disparities. Identify and compare conditions and outcomes across different populations in your community: members vs. non-members; differences by gender, race, income, or education level; homeowners vs. renters; proximity to a branch location; and so on.

- Prepare for future struggles. Even before the onset of the pandemic, research has suggested ongoing declines in well-being in the U.S. The COVID-19 crisis has exacerbated and accelerated these trends.[4]

Households and businesses were dependent on CARES Act aid, unemployment benefits, and support from financial institutions throughout the spring and summer of 2020. Many were effectively living off the exhaust fumes of these savings heading into the fall. Without further support, we expect to see increased levels of financial stress and impoverishment and a rising level of economic uncertainty and consumer discontent going into 2021.

Financial Well-being, Growth and Sustainability

The credit union business model has always been reflected in community prosperity. The financial well-being of credit union members feeds directly into the growth and sustainability of the credit union. By investing strategically in understanding and tracking their members’ well-being, credit unions can leverage this difference, centering the credit union value proposition around a commitment to improving the well-being of those they serve.

[1] Consumer Financial Protection Bureau, 2015, “Measuring Financial Well-being: A Guide to Using the CFPB Financial Well-being Scale.” https://files.consumerfinance.gov/f/201512_cfpb_financial-well-being-user-guide-scale.pdf

[2] Dodge, R., A.P. Daly, J. Huyton, and L.D. Sanders, 2012, “The Challenge of Defining Wellbeing,” International Journal of Wellbeing 2(3). https://www.internationaljournalofwellbeing.org/index.php/ijow/article/view/89

[3] Panchal, N., R. Kamal, K. Orgera, C. Cox, R. Garfield, L. Hamel, C. Muñana, and P. Chidambaram, 2020, “The Implications of COVID-19 for Mental Health and Substance Abuse,” Kaiser Family Foundation. https://www.kff.org/coronavirus-covid-19/issue-brief/the-implications-of-covid-19-for-mental-health-and-substance-use/

[4] See Gallup’s well-being index reports: https://news.gallup.com/topic/well_being_index.aspx