“Scams are on the rise.”

“Fraud is rampant.”

Financial fraud isn’t new. One of the first documented cases of financial fraud dates back to 300 B.C. and involves a corn merchant intent on sinking his ship to avoid paying back a loan. Today, fraud often involves millions of dollars, and with artificial intelligence at their disposal, fraudsters are frequently inventing dangerous new types of scams. Many have names creative enough to capture the imagination of even the most-pragmatically minded economist. (This one in particular was quite illustrative: “With ‘pig butchering’ scams on the rise, FBI moves to stop the bleeding.”) Credit union leaders are increasingly concerned about the prevalence and impacts of fraud and scams—on their members and their business.

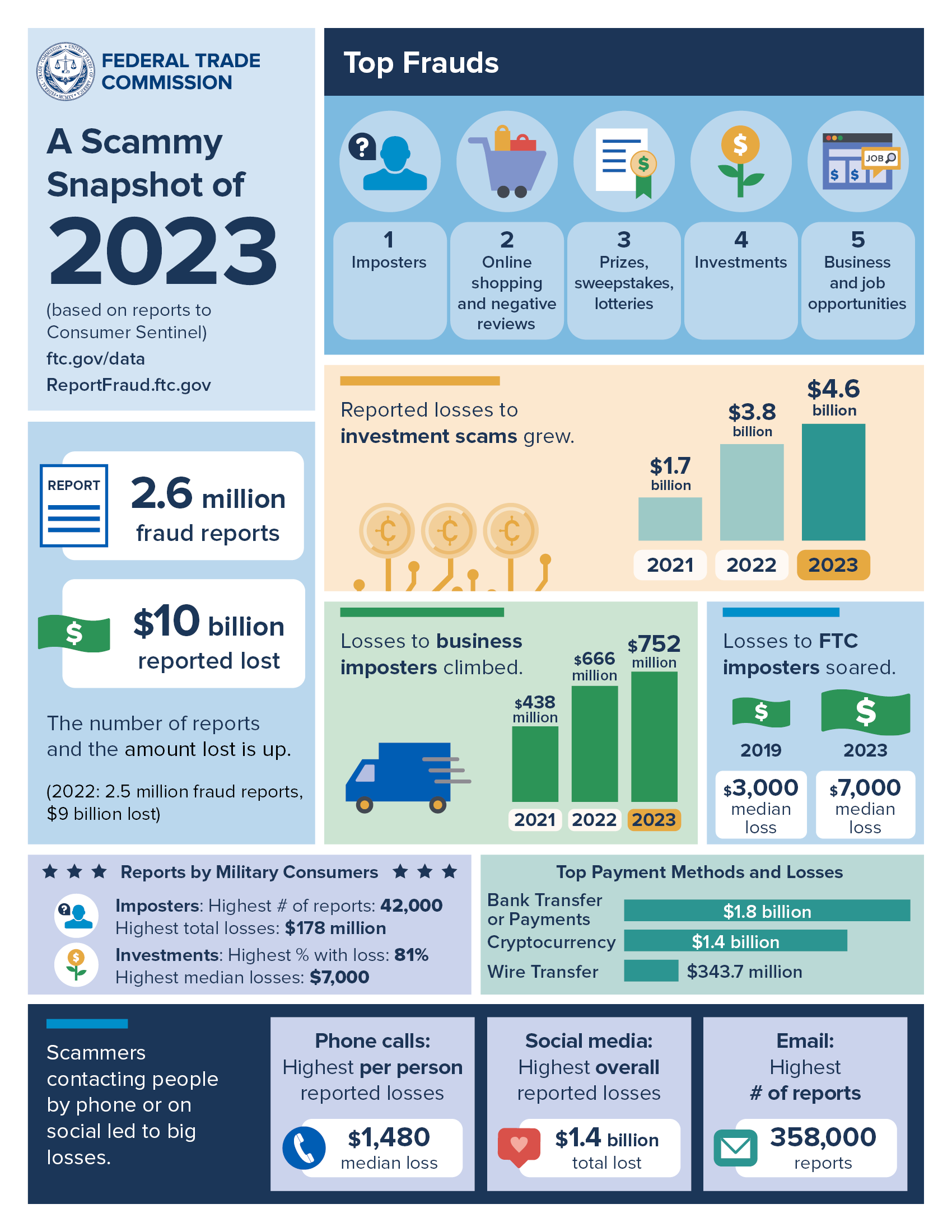

But what does “on the rise” actually look like? How “rampant” are scams and fraud across the consumer landscape? In their 2023 Data Book, the Federal Trade Commission reported 2.6 million reports of fraud filed, with $10 billion of lost money cumulatively reported by consumers. Stack that lost money together, and you’ll get a tower high enough to reach the International Space Station… and keep going for another 400 miles or so.

And yet, that lost money is still likely underrepresented. Feelings of shame, guilt, and grief are common among victims of fraud and likely result in underreporting, making it difficult to gauge the true impact of scams and fraud. Fraud and scams can occur across almost any channel: phone calls, texts, social media, or email. And while email scams generate the largest number of reports, it’s social media that results in the highest overall dollar loss, valued at $1.4 billion in 2023.

Fraud Across Generations

Financial fraud and scams can affect any person, anywhere. Previous research from Filene has highlighted the additional financial exploitation risk faced by vulnerable populations. Older individuals in particular face greater risk of falling victim to financial scams as they experience cognitive decline and growing isolation.

However, younger generations are not fraud-free. Social media channels account for the highest dollar loss, and despite being social media's most frequent users, younger generations may not be the scam-spotting-savants previously thought.

A Vox article from 2023 reports that younger generations have higher rates of falling victim to a variety of online scams, and a TIME article from earlier this year points to younger generations falling victim to “get-rich-quick” schemes they spot online, especially as they face inflation and high debt. Filene’s own research conducted in summer of 2023 (to be published soon!) shows that a third of credit union members under the age of 40 have already fallen victim to financial scams or fraud.

Filene’s own research conducted in summer of 2023 (to be published soon!) shows that a third of credit union members under the age of 40 have already fallen victim to financial scams or fraud.

Credit Union Members Disproportionately Affected

While financial fraud and scams can affect anyone, credit unions have recently been affected more than other industries. In Alloy’s most recent State of Fraud Benchmark Report, 79% of credit unions and community banks reported more than $500K in fraud losses—the highest of any group. (Note, however, that the report combined credit unions and community banks into a single category, which comprised 9% of the survey population).

Filene’s research confirms this trend from the member perspective. In a survey we conducted last year among credit union members and non-members, we found that 41% of credit union members were victims of financial scams or frauds, significantly higher than the 36% of non-members. And certain segments of credit union members are more affected than others.

In a survey we conducted last year among credit union members and non-members, we found that 41% of credit union members were victims of financial scams or frauds, significantly higher than the 36% of non-members.

When we looked through survey results through the lens of our new consumer segmentation model Member Voice, we found that credit union members who were Hopeful Help-Seekers and Overburdened Bystanders were more likely to report experiencing fraud and scams (44–45% versus 37–40%). This may also contribute to these groups’ financial struggles; these two segments are more likely to feel less financially confident and experience negative emotions when it came to their finances.

Results from Filene’s National Study, 2023

At Filene, we also took a deeper look at some of ways credit union members who have been victims of fraud/scams stand out from non-victims in their finances and provider preferences.

Personal Debt

1 in 3 credit union members who had experienced fraud/scams also reported struggling to cover their monthly expenses, and almost 50% said they were unsatisfied with their current financial household situation—a stark contrast with the much lower 36% of fraud-free members who report being unsatisfied.

At least some of this stress seems to be focused on debt—those who have previously experienced financial fraud/scams have slightly higher levels of debt (36% have $25K+ in debt) compared those who haven’t (32%). Where the difference becomes more stark, however, is how debt has affected the two groups. Those who’ve experienced fraud/scams have needed to cut back on spending (61% vs 52%), skipped payments on bills (21% vs 16%), or had debt sent to creditors (16% vs 9%) at higher rates than members who have never been victims.

While we can’t say for sure whether the financial fraud/scams these members experienced occurred before or after their experiences with debt, there is a clear connection—unmanaged debt and higher fraud/scam risk go hand-in-hand. Among those members who have been victims, over 40% reported that debt reduction was their top financial goal in the next 5 years.

Among those members who have been victims, over 40% reported that debt reduction was their top financial goal in the next 5 years.

What Members Want from Their Credit Union

On Filene’s study, we also asked credit union members what type of information they would like to receive from their financial institutions. We found that those who had experienced fraud/scams were more likely to look for a variety of communications at rates higher than their peers:

And while changes in credit score may be directly related to potential fraud prevention measures, other items on this list, however, seemingly speak to fraud and scam-affected members’ desire to keep in closer contact with their credit unions in general. Whether receiving account notifications or additional opportunities, they want to hear from their financial institutions.

What can credit unions do?

- Create shared solutions through collaboration: In a previous Thinking Forward post, we talked about the value of the credit union network working together to tackle the problem of fraud systemically. It is often cost-prohibitive for any single institution to address fraud at-scale, but through collaboration, there is an opportunity to invest in creative, systemic solutions.

- Help members manage and reduce debt: With the apparent connection between difficulties managing debt and being a victim of fraud/scams, helping members lower their debt (and their stress around it) could have a profound impact. It is integral that members see their credit unions as a trusted source for debt relief to help alleviate the chances of someone falling victim to debt relief scams.

- Utilize AI to fight fraud: While AI can accelerate fraud, it can also be utilized to accelerate efforts to fight it. America’s Credit Unions outlined some ways in which credit unions can think about using AI to fight fraud in a recent article.

- Provide resources for emotional stress caused by fraud: Those who have experienced financial debt are at greater risk for severe stress and anxiety. Providing training to credit union staff to equip them with the skills to recognize members in distress and provide resources could be extremely beneficial. The FINRA Foundation created a free resource to help empower consumers who have experienced fraud.

- Understand the scams/fraud landscape (and how it affects different generations): To fight fraud and scams effectively, we first need to understand the fraud/scam landscape. The Federal Reserve recently launched the ScamClassifier model to complement its previously launched FraudClassifier model to help this effort. Also, as credit unions seek to understand the different types of fraud/scams that exist and how to best address them, it is important to consider how fraud or scams appear to different generations of members. Education on recognizing fraud/scams across different channels can be beneficial—whereas recognizing email fraud may be more useful for older members, addressing awareness around social media scams may be more helpful for younger members.

Financial fraud is, unfortunately, not going away anytime soon, and its complexity is forever changing. But while fighting fraud and scams may feel like an uphill battle, it’s a necessary one. Remember that corn merchant from 300 B.C.? He was caught by sailors and guests aboard his own ship. With vigilance and proactivity, success against fraudsters and scammers is possible.

— AB

{kind=link}