Federal Student Debt: The Growing Problem

45 million adults in the US owe over $1.6 trillion in federal student debt. Federal student loans make up 92% of all student debt in the US and have characteristics that are quite different from the private student loans credit unions offer. More than doubling since the last recession, federal student debt is now the largest debt obligation for adults under 30 and by far the most problematic when comparing delinquency and default rates. Ten percent of borrowers were in default before the pandemic began and historically, up to forty percent of borrowers end up defaulting at least once over the life of their federal student loans.[1]

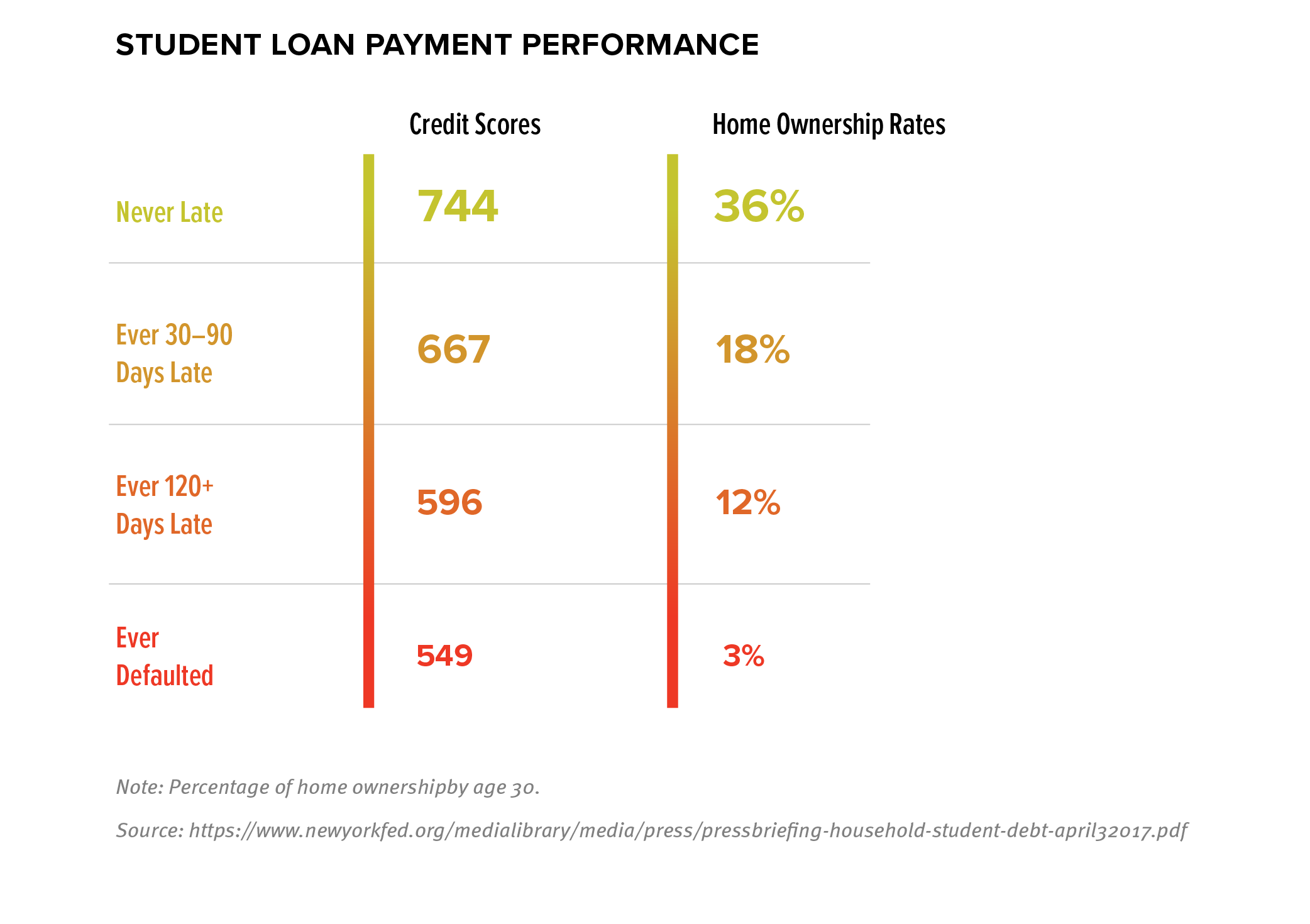

While 92% of student debt is held by the federal government, it has gotten so large and unwieldy that it is directly impacting credit unions business prospects with their members, whether they’re aware of it or not. In fact, research from the New York Federal Reserve shows that federal student loan payment history highly correlates with a student-borrower’s credit score and the chance of achieving important financial milestones like owning a home. Even missing a single payment correlates with an 80-point drop in a borrowers’ credit score, which can then limit access to other kinds of credit and impact people’s ability to rent a home, find employment, and more.

Viewing Federal Student Debt with a Behavioral Lens

While it is true that a lot of people have student debt (about 30% of all US adults[2]), it is also true that most borrowers owe less than $20,000 each in federal student loans. This may be surprising, if only because most news articles on this topic highlight examples of borrowers who are drowning in six figures of student debt. Moreover, and counterintuitively, the less a borrower owes when leaving school, the more likely they are to default on their federal student debt. Borrowers with less than $10,000 in outstanding debt make up 60% of all defaults.[3] These defaults crush credit scores and limit borrowers’ economic opportunity. Unfortunately, student loan default rates are inversely correlated with average neighborhood income. And the debt is exacerbating racial and gender wealth gaps.[4]

All borrowers have multiple options through the federal loan program that should enable them to keep their loans in good standing regardless of their income (or lack thereof). If we were robots with an infinite well of time and information, as classical economics typically assumes, one would look at the federal student debt repayment system as it’s designed today and assume close to a 0% default rate.

Yet we’re not robots; we’re human, with busy, complex lives, and the student debt repayment process is confusing and opaque, making it difficult for borrowers to navigate. The result is that borrowers often don’t take advantage of the free options and protections available to them, and end up in avoidable delinquency and default situations.

The Payment Cliff is Weeks Away

In March, the CARES Act automatically suspended nearly all federal student loan payments and set the loan interest rates to 0% until September 30. A Presidential Executive Order recently extended that reprieve until December 31, 2020 and then again until January 31, 2021. This was welcome and necessary relief, as in the months since loan payments were suspended, millions of Americans have experienced dramatic financial challenges.

But the interest rate and payment suspensions are coming to an end at the end of January, and we cannot assume that the ~30 million impacted individuals will be able to seamlessly resume their federal student loan payments, or that they will be behaviorally prepared to do so, even if their financial situation has remained steady. Behavioral science tells us that a nine-month grace period like the one just implemented can be an unintended trap. Though it offered much-needed short-term financial relief for many borrowers, 10 months is enough time for borrowers to have established new budget habits that don’t include monthly student debt payments.

The Opportunity for Credit Unions

Credit union executives nationwide have taken a number of measures to both help their members through this difficult financial period and to manage risk within their credit unions’ loan portfolios. Still, many acknowledge that is not enough to stop the anticipated flood of auto, mortgage, and other loan defaults, so they are dramatically increasing their loan-loss provisions.

Helping members manage their federal student loans will not only help them avoid the negative impact missed payments have on credit scores and financial well-being, but it will also improve members’ ability to repay their other debt obligations with their credit union. The federal government offers multiple repayment plan options that student-borrowers can take advantage of.

A credit union member with the median student debt owes roughly $20,000, meaning they’re paying roughly $200 per month. With the right digital guidance, they can move their loans onto an Income-Driven Repayment (IDR) plan and set their monthly payments to 10%-20% of their discretionary income. For many, this can lower their monthly payment by $100 or more. This:

- Ensures their federal loan payments will be affordable

- Frees up cash to cover other loan payments they have with their credit union

- Protects their credit score, putting them in a better position to pursue future financial services with their credit union as their income recovers.

If credit unions start paying attention to these opportunities now, they can help their members lower their monthly federal student loan payments and free up cash for members to use on their other debt obligations in 2021. That’s a clear win-win for the credit union and for its members.

Examples of Credit Unions Already Taking Action

Fortunately, it’s not too late to help your members navigate their federal student debt. Software services exist that can offer your members ongoing personalized guidance to manage their federal student loan payments (disclaimer - I am the founder and CEO of one such company, Nickels). These services can be quick and simple to launch, with members authorizing data integrations into their federal student loan servicer account(s) to enable the support they need while giving credit unions greater insight into their financial health.

For Lake Trust Credit Union, launching Nickels was as simple as sending an email. No data integration or IT integration was required. “We’re continuously looking for new ways to support our members’ financial health, particularly with the increased financial strain created by the pandemic. Helping our members manage their federal student debt is a natural extension of that mission and it was an easy topic for us to layer in to our member communication.’ said Andrea Mosher, SVP, Lending Solutions at Lake Trust Credit Union

COPFCU took things a step further, and embedded their new offering into their suite of services. “We try to make things as easy for our members as possible, so we were happy to embed the offering right into our website to make it more prominent for our members. It was straightforward, with just six lines of code to drop into a new webpage.” -Debbie Earley, Loan Manager at COPFCU.

There are options and protections available today to help credit union members lower their federal student debt payments. Helping them navigate those options will improve their financial health and unlock new business opportunities for credit unions in the process.

[1]https://www.brookings.edu/rese...

[2]https://thehill.com/policy/fin...

[3]https://assetfunders.org/wp-co...

[4]https://assetfunders.org/wp-co...